Managing your cash flow: how to get paid in advance

As any business owner will know, cash flow can kill your company – even if you’re successful. When the money comes in after the bills are overdue, you have to scramble. Luckily, there are some simple strategies for staying ahead of the cash flow curve. In addition to making your life less stressful, positive cash flow will make your business more enjoyable and truly profitable.

This article is all about the most important rule of all: Get Paid In Advance as much as possible.

Overview

Unfortunately, many people start their small businesses with the assumption that they need to extend credit to their clients. A handful of entrepreneurs somehow escape this mindset and never fall prey to the cash flow trap. As a general rule for success, you should collect as much money as possible in advance.

Here’s the basic problem: Timing.

And the basic reality: Money owed to you has a value less than one dollar per dollar.

The timing part is really the essence of cash flow. Let’s say you do $10,000 worth of work. Due to different client arrangements and paying habits, you might expect:

- $1,000 within the next week

- $3,000 more within the next two weeks

- $3,000 more within the next month

- $3,000 more within the next two months

In reality, you have bills to pay next week, the week after, this month, and next month. Getting “paid” $10,000 is great. But your creditors don’t care that you’ve extended credit to your customers. In this scenario, you’ll pay your employees and your landlord more than once before you get your money.

And the sad truth is that old money has less value. Money that’s more than 30, 60, 90 days old will probably be paid back with a “deal” that’s less than face value. I’ve talked to many consultants who are owed $25,000 or $50,000. Some even more. Every one of these folks would happily take 75% of the total just to get the money now.

If you operate that way on an on-going basis, then you need to build that into your rates. When you combine all clients, if you collect $90 for every $100 billed, then you need to adjust your budget to assume your effective billing rate is $90.

There are a handful of successful practices that can make all the difference with cash flow.

Start with the assumption that you’ll get paid in advance whenever possible. To be honest, making this change during (or at the end of) a recession may be the best possible timing. You won’t have to feel guilty about the change, and your clients will understand how tough things are.

Here are some basic “paid in advance” policies:

- Hardware and Software must be paid in advance before you order it from the distributor. Period.

- Project Labor must be paid in installments with a portion up front. The remainder should be paid on a schedule. The Schedule should be based on the completion of stages, not on a calendar schedule. If you give a calendar, make it an estimate and be clear that payments will be due upon the completion of stages.

- All Managed Service payments are due on the first day of the month. If the client pays by credit card of debit card, the card is run on the first day of the month. If the client pays by check, they must pay for three months at a time, due on the first of the first month.

- You should also include Hardware As A Service (HaaS), equipment rentals, remote monitoring and patch management, remote support, prepaid blocks of time, SPLA (Service Provider Licensing Agreement from Microsoft) or other licensing, and hosted services (spam filter, anti-virus, etc.). Anything that’s billed regularly is paid in advance.

So now you’re getting your money up front. There is a great joy in knowing that you’ve got the rent paid and all of the payroll covered. It really is a beautiful thing.

Timing is Everything

Let’s look at two common examples of cash flow. First, here’s what cash flow might look like if you have “terms” to be paid in arrears.

Next we’ll look at getting paid in advance. Note that the dollar amounts are the same.

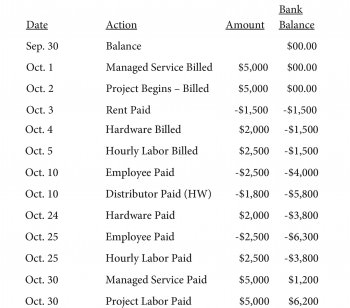

Example One: Arears

Terms: Labor due net 30 days. Project labor net 30 days. Hardware net 20 days. Rent due by the 5th. Employees paid on the 10th and 25th of each month.

Table 1: Payment in Arrears

In the end, you had a good month. You made $6,200 (we’re going to forget all of your other expenses for this example). But you were in the hole for MOST of the month – 22 days.

Where did that money come from? A line of credit loan? An investment from you, the owner? If you borrowed money, you need to pay it back with interest. And you don’t get to get paid on payday with the rest of your employees.

Now let’s see what it looks like when you get paid in advance.

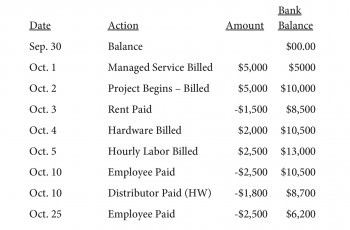

Example Two: Payment in Advance

Terms: Labor due in advance. Hardware due in advance. Rent due by the 5th. Employees paid on the 10th and 25th of each month.

Table 2: Payment in Advance

Of course you see the difference. You spend ZERO days with a negative balance. You borrowed zero dollars from your line of credit. You could even pay yourself $3,000 on the tenth of the month and still have plenty of money for everything. Then you could pay yourself another $3,000 on the twenty-fifth and still have money left over.

DO NOT think that this is just a made up example. This is real. You can do this. You should do this.

These are common, normal business practices and you should absolutely get paid in advance for (almost) everything you do. Any excuses you have for not doing this amount to fear. Please calm your fears.

Do it. Do it. Do it.

Every single coaching client I’ve had agree with me on this point: You will receive either zero client push-back or near-zero client push-back from these policies. They are simple and obvious.

And they can change your business.

Three take-aways from this chapter:

- Cash flow can kill your business. Get on top of it by getting paid in advance as much as possible.

- Old money has less value. When people owe you money, they often pay it back at a discount.

- Run real cash flow projections for your business – with options for payments in advance.

(Used with permission of Karl W. Palachuk, SmallBizThoughts.com)